activism

It’s only been half a year since President Trump issued an executive order to prevent the financial discrimination of socially stigmatized groups, which includes sex workers, crypto, and various other industries. This process happens through debanking, which is where groups are targeted and blocked from participating in the banking system. The core principles of this executive order have already been adopted by big monetary oversight agencies such as the OCC, the Federal Reserve, and the FDIC. Unfortunately, many institutions are already finding ways to circumvent these protections by inventing new loopholes with word games.

This executive order, otherwise known as Guaranteeing Fair Banking For All Americans, states that:

“It is the policy of the United States that no American should be denied access to financial services because of their constitutionally or statutorily protected beliefs, affiliations, or political views, and to ensure that politicized or unlawful debanking is not used as a tool to inhibit such beliefs, affiliations, or political views. Banking decisions must instead be made on the basis of individualized, objective, and risk-based analyses.”

Historically, reputational risk, which is vaguely defined, has been used by banks to discriminate against industries they don't like. They use affiliation to marginalized groups as a pretext for denying access to bank accounts, payment processors (such as PayPal and Venmo), loans, and more. This affects those who work with firearms, crypto, and adult entertainment, and more recently, those with particular political or religious beliefs.

When regulators removed (and prohibited) using reputational risk to debank groups, the sex worker community rightfully cheered and rejoiced. It felt like a champion had slayed the banking behemoth, and that the decades-long battle against financial discrimination would finally be over.

Unfortunately, this is no ordinary beast, it’s a hydra, where when it loses its head two more grow to replace it. After the executive order was issued, people lowered their guard and trusted the Wise platform to receive payments from adult sites such as Clips4Sale.

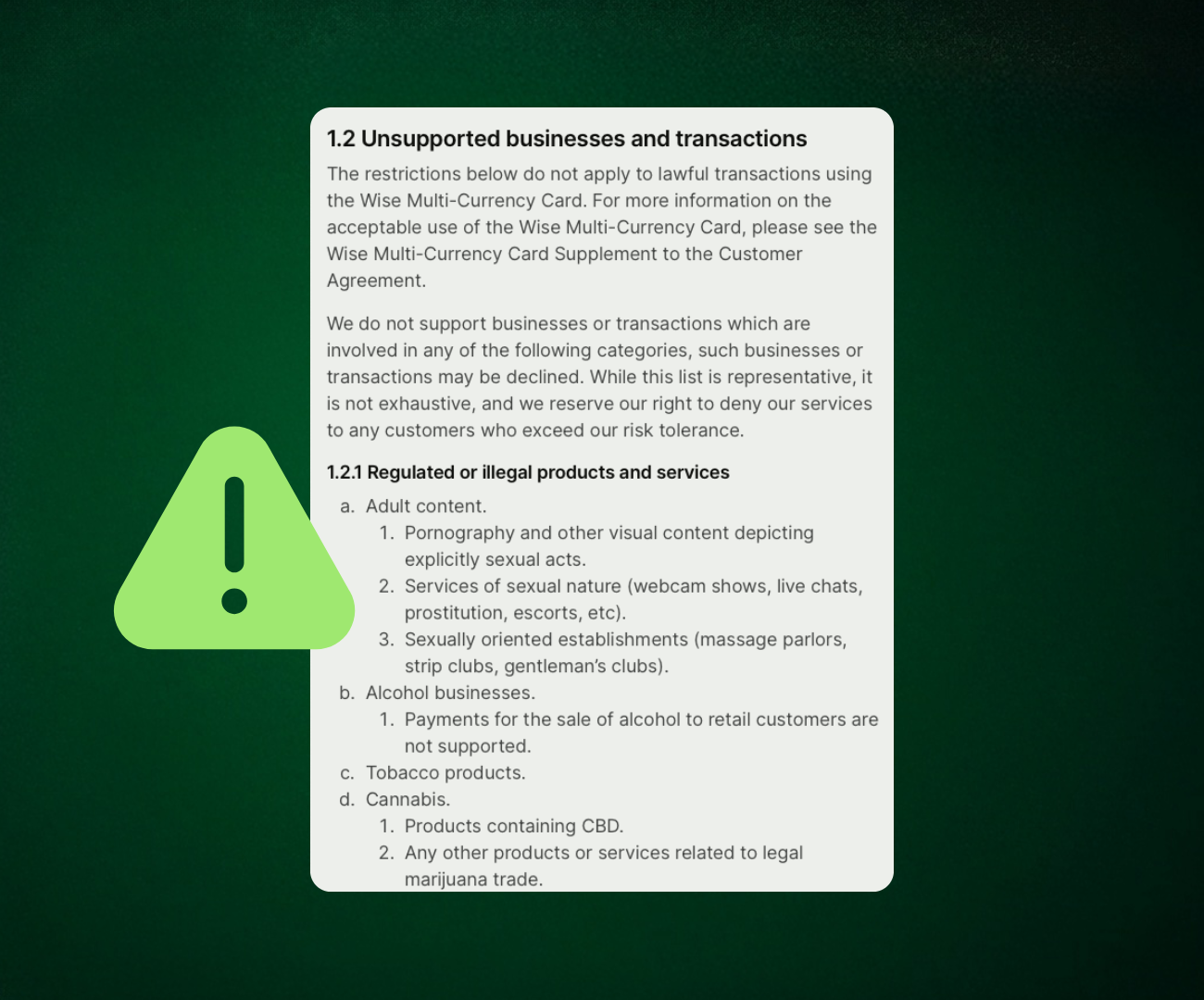

Wise is a UK-based money management and payment platform (similar to a Venmo) that is known for its ease of international currency exchange. They also have a US subsidiary that is a registered Money Service Business and registered with FinCen, which involves a rigorous licensure process that gives users confidence in the platform. This is perhaps why some users trusted it as a viable banking option and were later caught off guard.

In March 2025, Wise updated their Acceptable Use Policy to explicitly state that accounts connected to the adult industry would be banned. Five months later, when the executive order banned reputational risk, it rang across America like the end of a boxing match. Users flocked to the platform and didn’t take previously normal precautions to protect their privacy. Instead of using intermediary accounts to hide their connections to the adult industry, they processed revealing transactions and got deplatformed. In December 2025, Wise’s most recent updates reaffirmed that the adult industry was unwelcome on their platform.

So how is Wise justifying this continued financial discrimination? The same way everyone gets away with things in modern day America—via a loophole. The 'reputational risk’ that was the hydra’s head has now been replaced with “financial risk” and "compliance risk.”

So at this point it’s natural to ask, what the hell is the difference?

Financial risk is when an individual’s transactions show a pattern of behavior that indicates the account will operate at a loss, meaning that the merchant will pay more money to service it than it can earn. For example, a credit card user with a history of excessive chargebacks can cost the payment processor so much money it’s not worth it.

Compliance risk is when an individual’s actions show a pattern of behavior that might be associated with regulatory and legal violations. In these situations, the cost of compliance exceeds the value of operations.

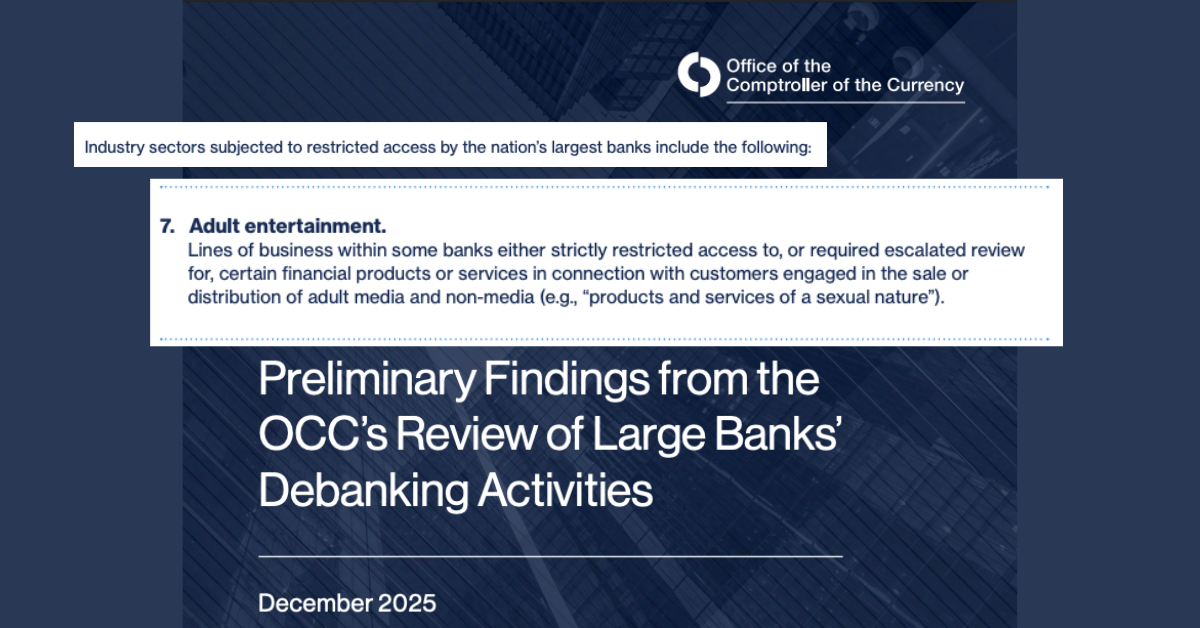

These two new risk positions shift the argument from targeting specific groups, such as the adult industry, to the individual, who gets specifically singled out and deplatformed. Unfortunately, many people are still getting debanked, with institutions running the reputational risk playbook under a different name. Fortunately, not everyone has been fooled, and this position has a way we can fight back. The OCC reported that it received over 100,000+ complaints, and for the first time in history, recognized the adult industry as a targeted group.

It is no secret that Washington and the banking sector use regulation to prevent businesses from operating. Risk arguments are often used to circumvent constitutional rights of undesirable industries and lead to censorship, and their enforcement creates moving goal posts. While courts have ruled that these positions do not not “technically” violate the constitution, the Free Speech Coalition argues that it violates it in all but name. These techniques were staples of Operation Chokepoint 2.0, and were specifically referenced in the executive order as a justification for why it had to be issued.

This is not to say institutions are the enemy. Ironically, this loophole is a valid strategy for monetary institutions to protect their money and themselves, and it is often broadly applied to mitigate corporate risk. Banning entire industries has historically been the safest, easiest, and most affordable path to avoid regulatory minefields. For companies to feel safe to abandon their compliance safety blankets, we must help them reassess their strategies and encourage them to pursue mutually beneficial opportunities.

The executive order and institutions have laid the groundwork to turn discriminatory tactics back on the enforcers. Each time that they deplatform a user, companies are required to create a record and justification, and must comply with strict filing requirements and deadlines. Even if an individual feels powerless, every challenge costs them money in compliance, and will eventually tip the scales to make discrimination prohibitively expensive. On that note, for anyone who has been impacted by Wise, click here to read our step-by-step guide on how to submit your complaint.

In this case, complaining to the manager can actually be effective. Companies must answer to regulators who answer to elected officials. As strange as it sounds, politicians track letters and complaints by zip code and issue, and make voting decisions accordingly to protect their careers. Everyone using US financial products has a right to complain to the Consumer Protection Financial Bureau (CFPB), which can be filed here. CFPB is known to be responsive, and typically provides a response within 15 days, and with resolutions within 60 days.

For the manager’s manager, this official government site can be used to find and reach out to elected officials who can help advocate for future legislation. Florida, Tennessee, and Texas have fair access and anti-debanking laws that view debanking as a crime. In these cases, it’s useful to contact the State Attorney General for compliance. Preferred contact methods vary from phone numbers to forms, and offices all have a mailing address to receive letters. We have created a debanking template letter to make this process quick and simple.

Always remember, everyone’s story makes a difference, even if it’s not immediately heard. If you are directly impacted, please reach out to the FSC and tell them your story. It is only when we get to the heart of these injustices and share details at the personal level that we become more than a number and our voices can be heard. The FSC is a tremendous leader in the adult advocacy space and is constantly in front of Congress lobbying for the rights of all. Each personal account has the potential to move the public and fight in DC. By sharing your story, you help not only yourself, but also the industry, and everyone that believes in fairness, compassion, freedom, and accountability.