Click through this SpankByte to see what steps you can take to preserve any evidence and bolster your chances of getting your funds/account back from Wise. We created this guide specifically for those of you who have recently been deplatformed by Wise simply for being associated with the adult industry. A lot of this information is relevant for other debanking situations, but this edition is dedicated to the recent issues surrounding Wise.

Information on the recent Wise deplatforming, plus a step-by-step creator’s guide on the next steps to take after debanking occurs.

Assessing the Risk Assessment

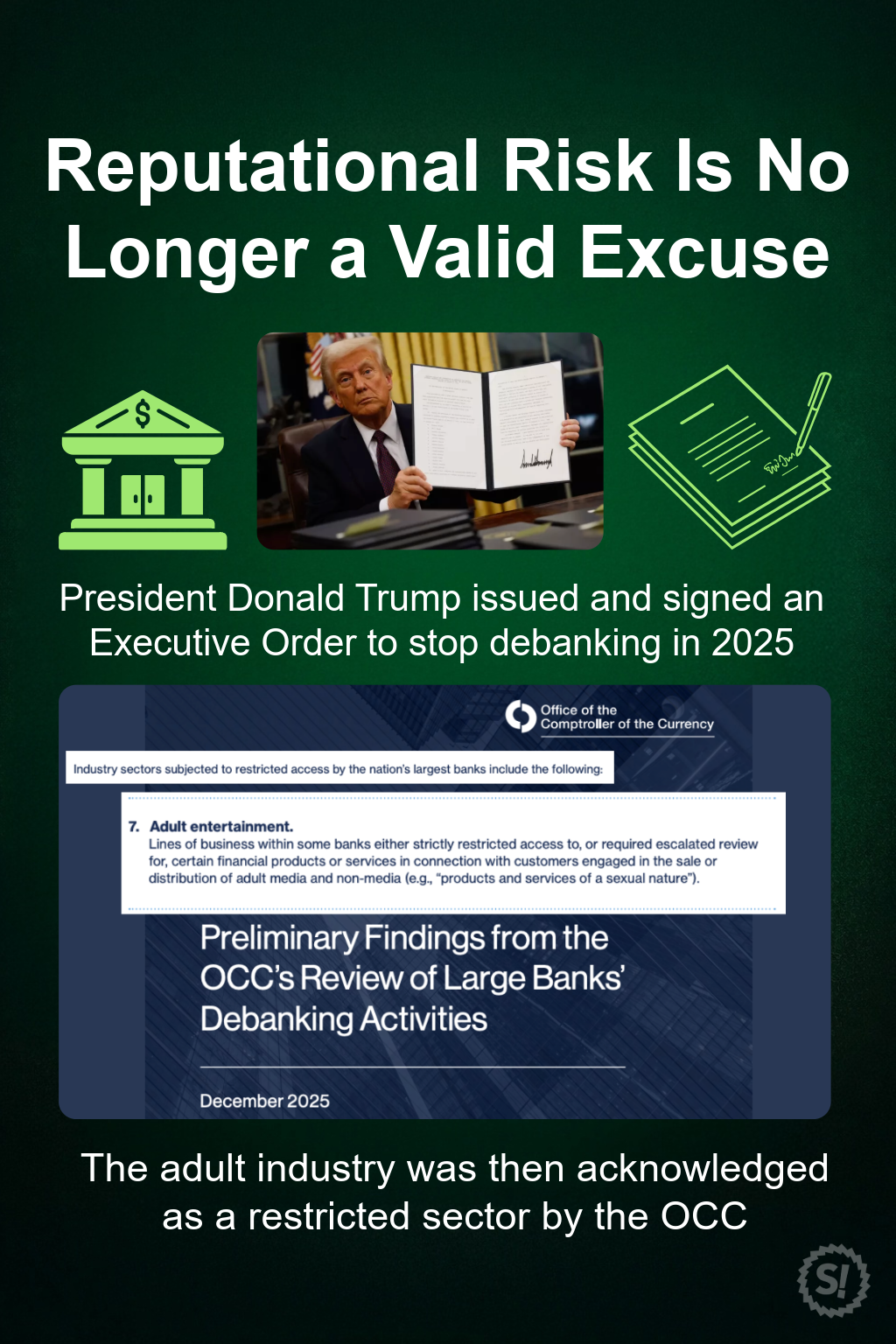

In August 2025 an executive order banning monetary and financial institutions from deplatforming users over reputational risk was signed and invoked.

They are still allowed to deplatform individuals based on their own specific financial and compliance risks, such as if your account has a history of chargebacks or interactions with sanctioned entities and individuals.

What they are not allowed to do is deplatform someone for being part of a taboo industry, and then claiming that entire industry is a financial and compliance risk.

Each account must be judged independently on its own merits. This is the entire spirit of the executive order. Its whole purpose is to prevent declaring someone guilty by association as justification for financial discrimination.

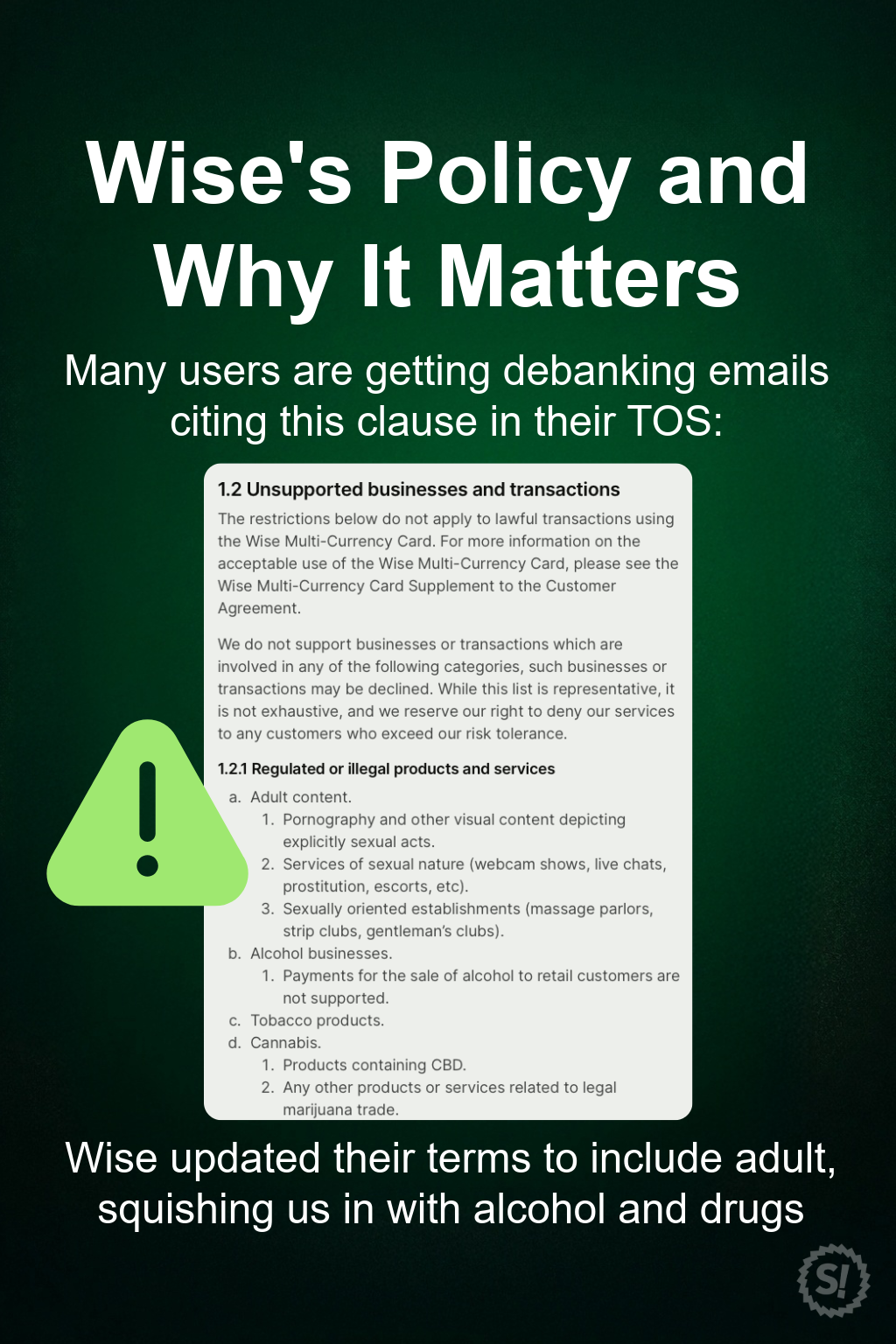

Why Definitions Matter

Since access to financial and monetary technology is essential to survive and participate in a modern economy, it is crucial that the ban on debanking people for reputational risk be taken seriously.

Wise is well within their rights to refuse service based on financial and compliance risk tolerances of individual accounts, but their denial letters that we have seen seem to indicate that their risk tolerances are based on industries and not individuals.

We strongly believe that this is wrong, and that the spirit of the executive order prohibiting reputational risk is being ignored.If you have been personally affected by Wise due to your association with the adult industry, the rest of this guide is tailored specifically for you.

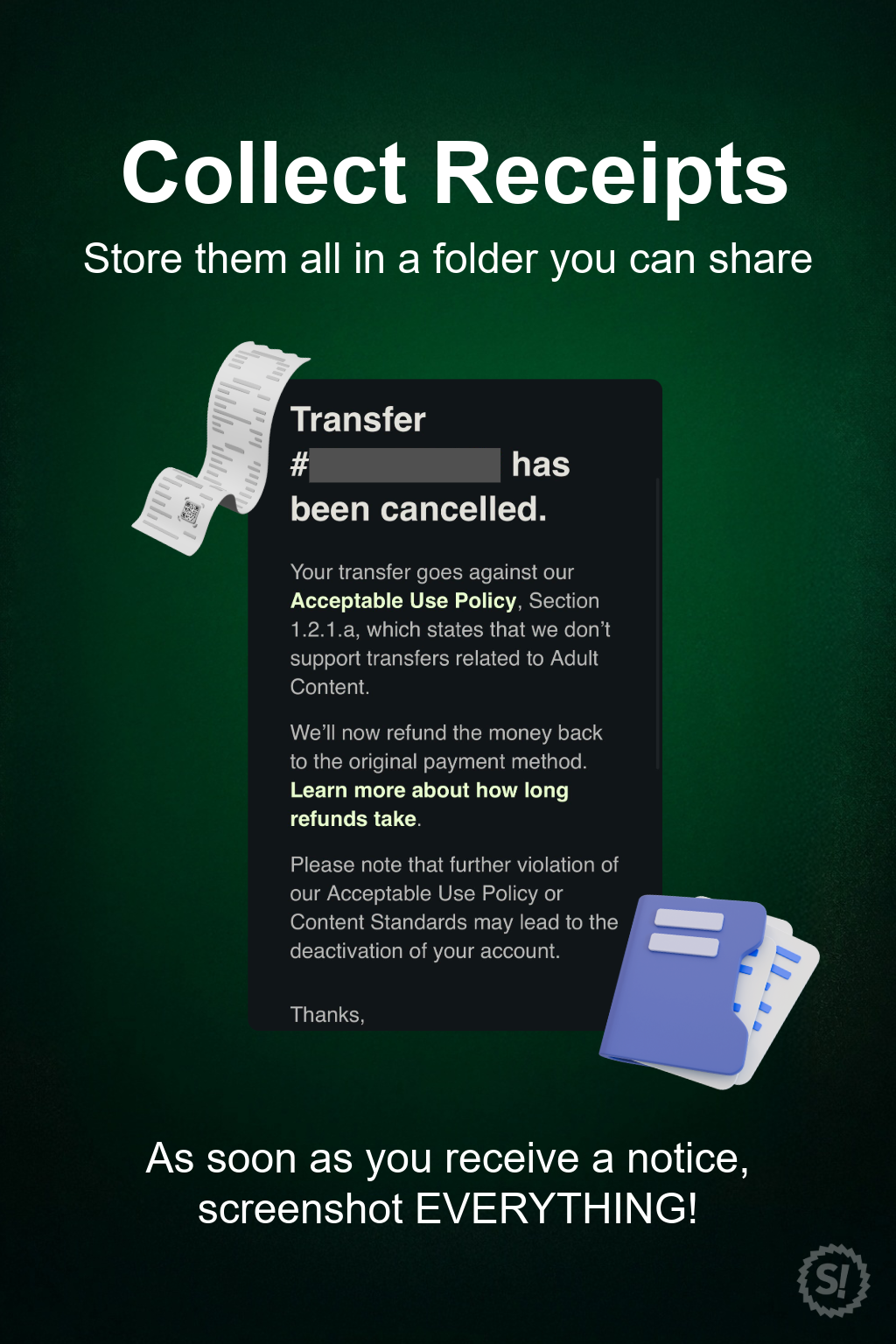

Collect Receipts

If you get a message like “We do not support transfers related to Adult Content,” treat it as a compliance action, and preserve everything before you click around.

Collect your “receipts” and Create a folder (Google Drive/Dropbox/PC) and save:

1) The Wise notice itself (most important)

- Screenshot of the exact message (include date/time if visible)

- Screenshot of the page showing it’s from Wise (app UI / email header)

2) Account + funds proof

- Screenshot of your Wise balance(s) and any “restricted” banner

- Screenshot of failed transfers (error screen + amount + destination)

- Any emails from Wise about account closure/restriction

3) Transaction IDs + reference info

- Wise transfer ID / reference number

- Dates, amounts, currencies, recipients

4) The policy they’re citing

- Screenshot or saved PDF of the Wise Acceptable Use Policy section where Adult content is listed

- If you use Wise Business, also save the Wise Help page that says Wise doesn’t work for businesses involved in adult content

5) Your “lawful business” context (keep it simple)

- A short statement: “I am a legal adult creator / service provider; income is lawful.”

- Optional: business registration basics if you have them (LLC name, EIN, etc.)

Withdraw Remaining Funds (If you can!)

Do NOT keep money sitting in your Wise account if you still have access.

If you can still move funds:

- Withdraw to your linked bank

- Transfer to another account you control

- Avoid repeated or partial retries that create new flags (keep it minimal)

If you can’t move funds:

- Continue to the next step immediately.

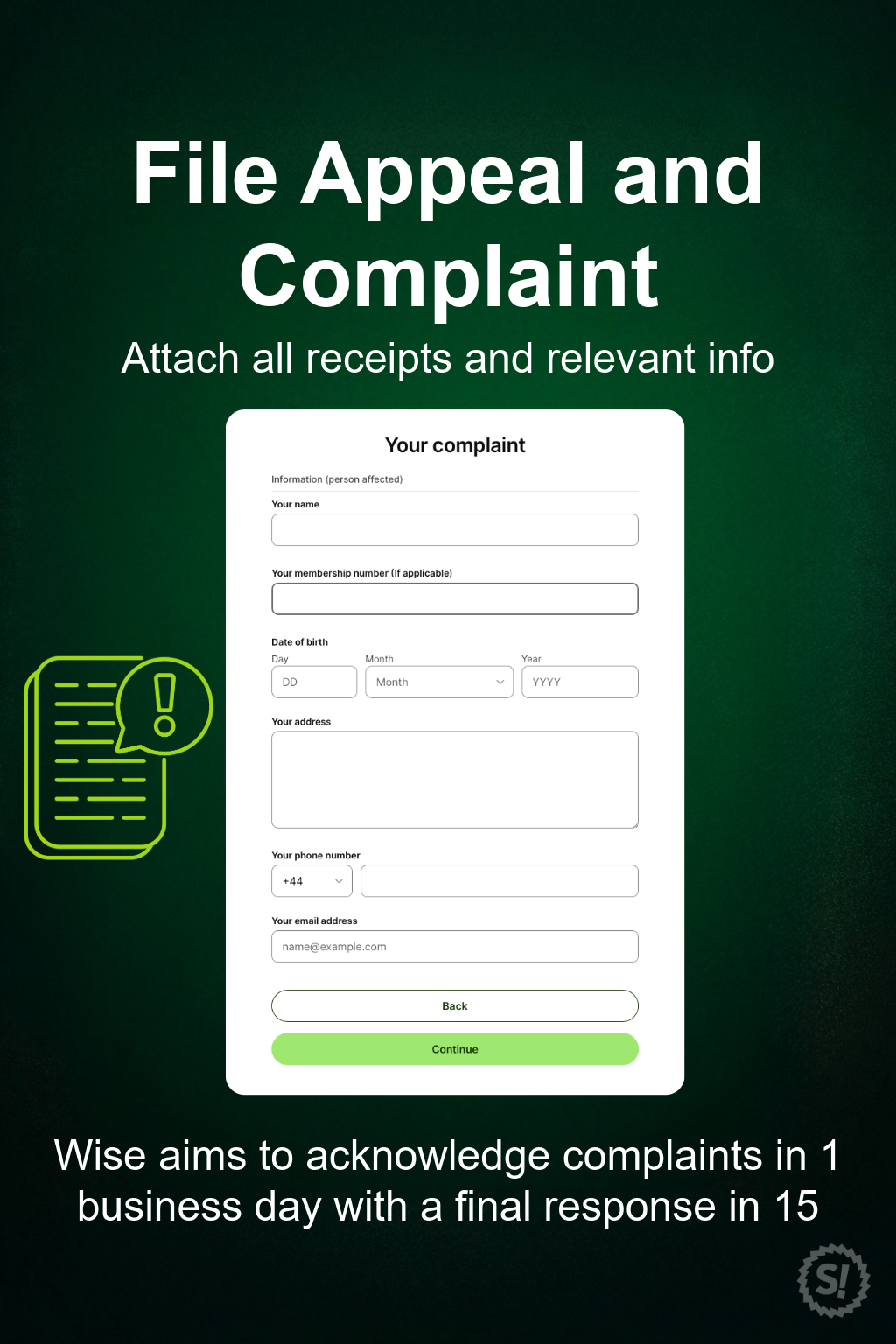

File Appeal and Complaint

File an appeal with Wise first if you can, and then file an official complaint.

Wise has a formal complaints process and states they aim to:

- acknowledge within 1 working day

- provide a final response typically within 15 calendar days

Link to appeal: https://wise.com/appeals

Link to file a complaint: https://wise.com/help/contact/forms/complaints

Escalate the Issue

If you’re in the U.S., file a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov/complaint. (CFPB complaints apply to U.S. users or U.S.-based accounts. If you’re outside the U.S., Wise has a comprehensive list of who you can contact based on your location here.)

Why this matters:

- CFPB routes complaints to the company for response and can share with relevant agencies

- This forces a tracked, written reply and builds a pattern record.

What to include in the CFPB complaint:

- “Funds inaccessible / transfer blocked”

- “Restriction based on ‘Adult Content’ per TOS”

- “No meaningful notice / no appeal / unable to access funds (if applicable)”

- “Request: release funds + written explanation + appeal path (if applicable)”

Upload all of your “receipts” from earlier, including your final response from Wise.

File with your State Attorney General (or state financial regulator)

U.S. users should do this especially if your funds are held, access is blocked for days, or if multiple people report the same thing.

Your AG complaint should focus on:

- inability to access your own funds

- unclear process/timeline

- harm to livelihood

- abrupt policy enforcement

FInd your AG: https://www.naag.org/find-my-ag/

If you’d like to share your experience with banking discrimination you can also contact the Free Speech Coalition: https://www.freespeechcoalition.com/share-your-banking-discrimination-story